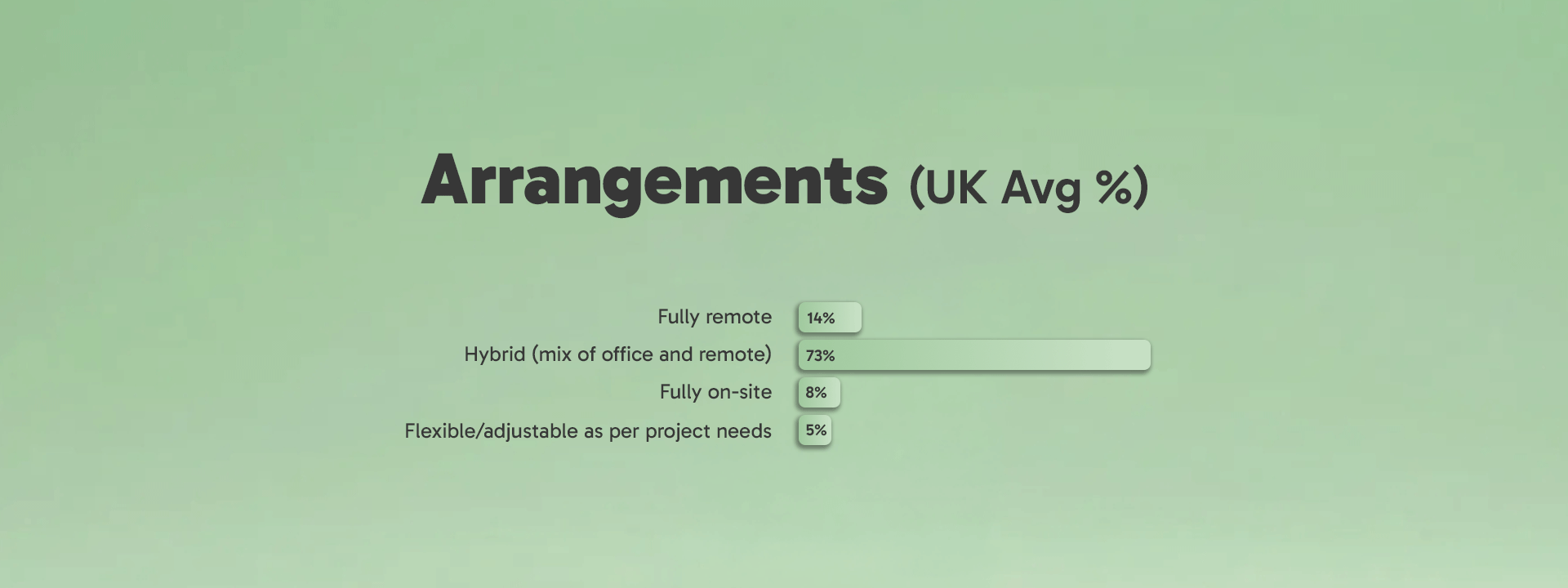

Hybrid working has evolved from an emergency response into the default operating model for much of the UK finance profession. What was once considered a temporary compromise has become the standard expectation for experienced accountants, auditors and tax professionals. The overwhelming preference for hybrid arrangements demonstrates that most organisations have found a practical balance between collaboration, client service and individual productivity. Rather than debating whether hybrid works, most firms are now focused on refining how it works best.

The relatively small proportion of fully remote roles also tells an important story. While many candidates continue to value complete flexibility, employers increasingly recognise the importance of face-to-face coaching, team cohesion, client interaction and knowledge sharing - particularly for developing junior professionals. Audit firms, in particular, continue to rely on in-person collaboration to transfer technical knowledge that simply cannot be replicated entirely through video calls. The result is a market settling into pragmatic realism rather than ideological extremes.

The organisations creating unnecessary friction are those attempting to reverse this trend through rigid return-to-office mandates without a compelling commercial reason. Candidates increasingly interpret inflexible policies as indicators of wider cultural issues, including trust, leadership style and employee autonomy. In a highly competitive labour market, hybrid working is no longer viewed as a discretionary benefit. It has become part of the psychological contract between employer and employee, and organisations that fail to recognise this risk reducing both their recruitment appeal and their retention capability.